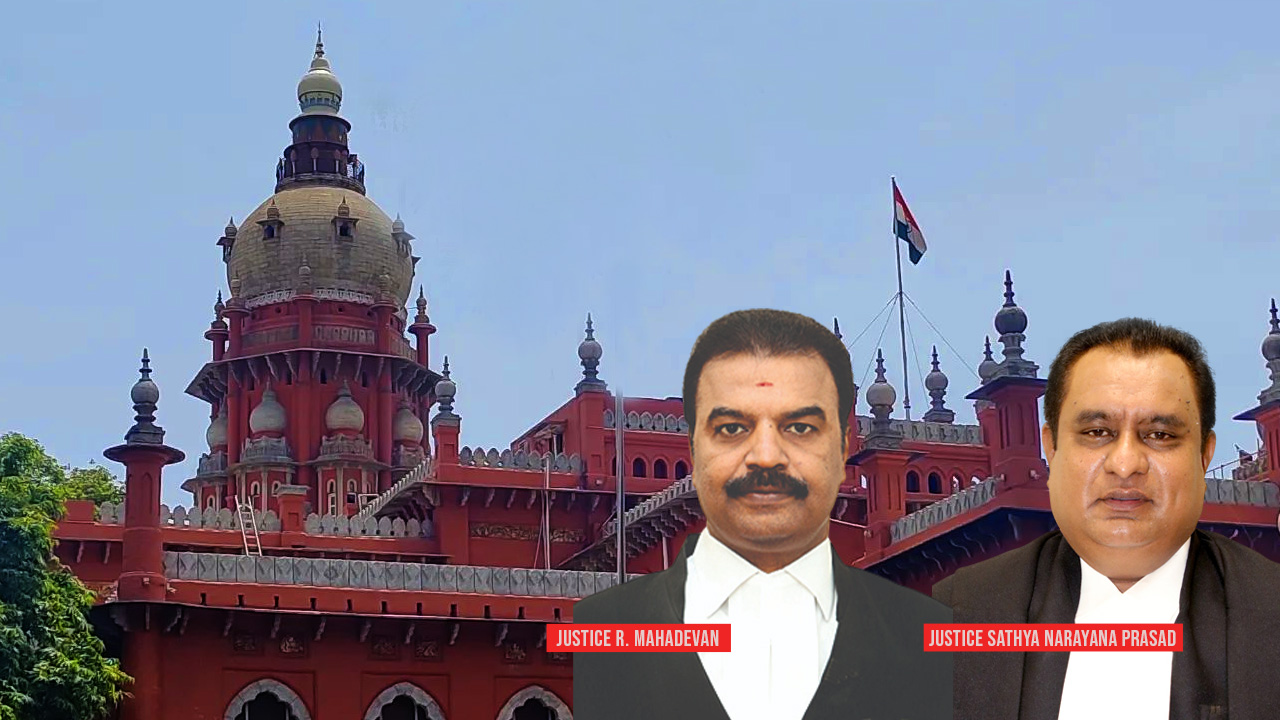

TPO To Mandatorily Pass Order Determining Arm's Length Pricing Within 60 Days: Madras High Court

Live LawThe Madras High Court bench of Justice R.Mahadevan and Justice J.Sathya Narayan Prasad has held that the transfer pricing officer must mandatorily pass the order determining arm's length pricing within 60 days. The Deputy Commissioner of Income Tax passed the order under Section 92CA of the Income Tax Act, which, according to the assessee, was passed, after the time limit prescribed for passing orders until 31.10.2019. The department contended that where there was no reference made to a transfer pricing officer, the time limit for completion of the assessment is 21 months from the end of the assessment year, as contemplated under Section 153 of the Income Tax Act, and in that event, the last date for passing an order of assessment in this case will be 31.12.2018. As per Section 92CA, a Transfer Pricing Order has to be passed 60 days prior to the date on which the time limit provided under Section 153 of the Act expires.

History of this topic

Direct Tax Weekly Round-Up: 21 To 27 July 2024

Live Law

Final Assessment Made By AO After Expiry Of One Month Of Receiving Directions From Dispute Resolution Panel, Is Time Barred: Chennai ITAT

Live Law

Period Of Limitation Under S.153 Of Income Tax Act Applies To Remand Proceedings : Madras HC

Live LawDiscover Related

![[Income Tax] No Substantial Question Of Law Arises If Perversity Cannot Be Shown In Order Passed By Tribunal: Allahabad High Court](https://www.livelaw.in/h-upload/2024/10/31/568956-allahabad-high-court-prayagraj.jpg)

![[S.73(10) UPGST] Time Extension Notification Dated 24.04.2023 Valid Only From 31.03.2023, Not Before: Allahabad High Court](https://www.livelaw.in/h-upload/2024/11/20/572156-lucknow-bench-allahabad-high-court-lucknow.jpg)

![[Direct Tax Vivaad Se Vishwas Act] Review Plea Against SLP Constitutes "Disputed Tax" U/S 2(i)(j): Delhi High Court](https://www.livelaw.in/h-upload/2024/09/11/560539-justice-yashwant-varma-justice-ravinder-dudeja-delhi-high-court.jpg)